If you’re making a long-term investment in an asset or project, it’s important to keep a close eye on your plans and budgets. Accounting Rate of Return (ARR) is one of the best ways to calculate the potential profitability of an investment, making it an effective means of determining which capital asset or long-term project to invest in. But how do you do an ARR calculation? Find out everything you need to know about the Accounting Rate of Return formula and how to calculate ARR, right here.

What is ARR?

Accounting Rate of Return (ARR) is the percentage rate of return that is expected from an investment or asset compared to the initial cost of investment. Typically, ARR is used to make capital budgeting decisions. For example, if your business needs to decide whether to continue with a particular investment, whether it’s a project or an acquisition, an ARR calculation can help to determine whether going ahead is the right move.

What is the Accounting Rate of Return formula?

The Accounting Rate of Return formula is as follows:

ARR = average annual profit / average investment

Of course, that doesn’t mean too much on its own, so here’s how to put that into practice and actually work out the profitability of your investments.

How to calculate ARR

Doing an ARR calculation is relatively simple. Here’s what you need to do to calculate ARR:

First off, work out the annual net profit of your investment. This will be the revenue remaining after all operating expenses, taxes, and interest associated with implementing the investment or project have been deducted.

If the investment is a fixed asset, such as property, you’ll need to work out the depreciation expense.

Then, to arrive at the final figure for annual net profit, simply subtract the depreciation expense from your annual revenue figure.

Finally, you simply divide the annual net profit by the initial cost of the asset or investment. The calculation will show a decimal, so multiply the result by 100 to see the percentage return.

If you’re not comfortable working this out for yourself, you can use an ARR calculator online to be extra sure that your figures are correct. EasyCalculation offers a simple tool for working out your ARR, although there are many different ARR calculators online to explore.

ARR Calculation – an example

Here’s an example of how to use the Accounting Rate of Return formula in the real world. A Company wants to invest in new set of vehicles for the business. The vehicles cost £350,000 and would increase the company’s annual revenue by £100,000, as well as the company’s annual expenses by £10,000. The vehicles are estimated to have a useful shelf life of 20 years, with no salvage value. So, the ARR calculation is as follows:

Average annual profit = £100,000 – £10,000 = £90,000

Depreciation expense = £350,000 / 20 = £17,500

True average annual profit = £90,000 – £17,500 = £72,500

ARR = £72,500 / 350,000 = 0.2071 = 20.71%

So, in this example, for every pound that your company invests, it will receive a return of 20.71p. That’s relatively good, and if it’s better than the company’s other options, it may convince them to go ahead with the investment.

How to calculate Accounting Rate of Return in Excel?

To keep track of ARR more comprehensively, it may be a good idea to use a spreadsheet tool like Microsoft Excel. If you’re using Excel to calculate ARR, follow these simple steps:

In A1, write ‘Year’.

In C1-G1, write 1, 2, 3, 4, 5 (assuming a five-year project).

In A2, write ‘Net Income’.

In C2-G2, write the net annual income for each year.

In A3, write ‘Initial Investment’.

In B3, write the initial investment for the project.

In A4, write ‘Salvage Value’.

In B4, write the salvage value, if any.

In A5, write ‘ARR’.

In B5, write =AVERAGE(C2:G2)/AVERAGE(B3:B4).

Press enter to calculate ARR.

ARR will now show in B5.

Remember that you may need to change these details depending on the specifics of your project. For example, your project may last longer than five years. Overall, however, this is a simple and efficient method for anyone who wants to learn how to calculate Accounting Rate of Return in Excel.

We can help

If you’re making long-term investments, it’s important that you have a healthy cash flow to deal with any unforeseen events. Find out how GoCardless can help you with ad hoc payments or recurring payments .

Collect payments in Europe? Read our guide to SEPA Payments

Everything you need to know about SEPA Payments: How they work, Pros & Cons, How to Access, Costs, Timings and more.

GoCardless makes it easy to collect recurring payments

The simplest rate of return to calculate is the accounting rate of return (ARR). This is a very fundamental calculation to determine how much value an investment generates for the corporation and its owners, the stockholders. It requires only two pieces of information: the amount of earnings before interest and taxes (EBIT) generated by the project and the cost of the investment.

Once you know those two things, the calculation goes like this:

ARR = EBIT attributed to project / Net investment

The accounting rate of return is calculated by dividing the amount of EBIT generated by the project by the net investment of the project. This calculation tells you the proportion of net earnings before taxes that you’re generating for the investment cost.

This calculation is usually done on a year-by-year basis. Note that because this equation doesn’t take multi-period variables into consideration, you have to calculate it anew for each period (usually a year). So, in year 1, you might calculate a –3 percent rate of return.

That sounds bad, but if you’re talking about the investment on developing a whole new product line, you need to consider that sales are usually slow during the first year. By year 3, you might expect a 2 percent rate of return, and so forth.

You may be asking how to determine the amount of EBIT to attribute to a given project! The answer isn’t too bad. Basically, you just go through the steps of developing an income statement, but only for the new project. Find out how many sales this new line or product is generating, and then subtract the costs of operating the project. That’s simple, right?

When your capital investment is just a single step in the production process, determining how much value is being added by that step takes a little more work. Basically, you have to break down the entire production process into its individual contributing steps. The total production process is 100 percent of the final product.

There are a couple ways to determine what percentage of the production process a single step constitutes. One way is to simply use a proportion of the total cost of production. Sure, this method is easy, but there’s a better way:

You can do something called transfer pricing, which estimates the market value of each step in the process by doing some research to find out how much it would cost to hire some other company to do that step. This method helps you in two ways:

It helps you do your capital budgeting by determining the amount of added value for that single step and the amount of EBIT you can attribute to that step, to make sure that the investment will actually generate a positive return on investment.

It determines the fair market value of performing that step to see whether your company is being financially efficient. If some other company can perform that step better or more cheaply, you should probably outsource that step to the other company.

If you know the lifespan of the project or machine, you can forecast the rate of return you experience each year. Whether you’re successful at this forecast or not will depend entirely on how closely your forecasts match the actual rate of returns, of course, but you can still do these forecasts.

The total rate of return on the investment is the total EBIT generated by that investment divided by the cost of the investment. The revenues used to calculate EBIT include all the revenues that investment generates over its entire life, plus the final revenue generated using its salvage or scrap value. The final revenue generated by any project is its scrap or salvage value.

What Is the Accounting Rate of Return – ARR?

The accounting rate of return (ARR) is the percentage rate of return expected on investment or asset as compared to the initial investment cost. ARR divides the average revenue from an asset by the company’s initial investment to derive the ratio or return that can be expected over the lifetime of the asset or related project. ARR does not consider the time value of money or cash flows, which can be an integral part of maintaining a business.

Rate of Return

The Formula for ARR

A R R = A v e r a g e A n n u a l P r o f i t I n i t i a l I n v e s t m e n t ARR = frac

How to Calculate the Accounting Rate of Return – ARR

- Calculate the annual net profit from the investment, which could include revenue minus any annual costs or expenses of implementing the project or investment.

- If the investment is a fixed asset such as property, plant, or equipment, subtract any depreciation expense from the annual revenue to achieve the annual net profit.

- Divide the annual net profit by the initial cost of the asset, or investment. The result of the calculation will yield a decimal. Multiply the result by 100 to show the percentage return as a whole number.

What Does ARR Tell You?

The accounting rate of return is a capital budgeting metric useful for a quick calculation of an investment’s profitability. ARR is used mainly as a general comparison between multiple projects to determine the expected rate of return from each project.

ARR can be used when deciding on an investment or an acquisition. It factors in any possible annual expenses or depreciation expense that’s associated with the project. Depreciation is an accounting process whereby the cost of a fixed asset is spread out, or expensed, annually during the useful life of the asset.

Depreciation is a helpful accounting convention that allows companies not to have to expense the entire cost of a large purchase in year one, thus allowing the company to earn a profit from the asset right away, even in its first year of service. In the ARR calculation, depreciation expense and any annual costs must be subtracted from annual revenue to yield the net annual profit.

Key Takeaways

- ARR is helpful in determining the annual percentage rate of return of a project.

- ARR can be used when considering multiple projects since it provides the expected rate of return from each project.

- However, ARR does not differentiate between investments that yield different cash flows over the lifetime of the project.

Example of How to Use the Accounting Rate of Return – ARR

A project is being considered that has an initial investment of $250,000 and it’s forecasted to generate revenue for the next five years. Below are the details:

- initial investment: $250,000

- expected revenue per year: $70,000

- time frame: 5 years

- ARR calculation: $70,000 (annual revenue) / $250,000 (initial cost)

- ARR = .28 or 28% (.28 * 100)

The Difference Between ARR and RRR

As stated, the ARR is the annual percentage return from an investment based on its initial outlay of cash. However, the required rate of return (RRR), also known as the hurdle rate, is the minimum return an investor will accept for an investment or project, that compensates them for a given level of risk.

RRR can vary between investors because investors have different risk tolerances. For example, a risk-averse investor would likely require a higher rate of return from investment to compensate for any risk from the investment. It’s important to utilize multiple financial metrics including ARR and RRR, in determining if an investment is worth it.

Limitations of Using the Accounting Rate of Return – ARR

The ARR is helpful in determining the annual percentage rate of return of a project. However, the calculation has its limitations.

ARR doesn’t consider the time value of money (TVM). The time value of money is the concept that money available at the present time is worth more than an identical sum in the future due to its potential earning capacity. In other words, two investments might yield uneven annual revenue streams. If one project returns more revenue in the early years and the other project returns revenue in the later years, ARR does not assign a higher value to the project that returns profits sooner, which could be reinvested to earn more money.

The accounting rate of return does not consider the increased risk of long-term projects and the increased uncertainty associated with long periods.

Also, ARR does not take into account the impact of cash flow timing. Let’s say an investor is considering a five-year investment with an initial cash outlay of $50,000, but the investment doesn’t yield any revenue until the fourth and fifth year. The investor would need to be able to withstand the first three years without any positive cash flow from the project. The ARR calculation would not factor in the lack of cash flow in the first three years.

Accounting CPE Courses & Books

The accounting rate of return is the expected rate of return on an investment. The calculation is the accounting profit from the project, divided by the initial investment in the project. One would accept a project if the measure yields a percentage that exceeds a certain hurdle rate used by the company as its minimum rate of return. The formula for the accounting rate of return is:

Average annual accounting profit ÷ Initial investment = Accounting rate of return

In this formula, the accounting profit is calculated as the profit related to the project using all accruals and non-cash expenses required under the GAAP or IFRS frameworks (thus, it includes the costs of depreciation and amortization). If the project involves cost reduction instead of earning a profit, then the numerator is the amount of cost savings generated by the project. In essence, then, profit is calculated using the accrual basis of accounting, not the cash basis. Also, the initial investment is calculated as the fixed asset investment plus any change in working capital caused by the investment.

The result of the calculation is expressed as a percentage. Thus, if a company projects that it will earn an average annual profit of $70,000 on an initial investment of $1,000,000, then the project has an accounting rate of return of 7%.

There are several serious problems with this concept, which are:

Time value of money. The measure does not factor in the time value of money. Thus, if there is currently a high market interest rate, the time value of money could completely offset any profit reported by a project – but the accounting rate of return does incorporate this factor, so it clearly overstates the profitability of proposed projects.

Constraint analysis. The measure does not factor in whether or not the capital project under consideration has any impact on the throughput of a company’s operations.

System view. The measure does not account for the fact that a company tends to operate as an interrelated system, and so capital expenditures should really be examined in terms of their impact on the entire system, not on a stand-alone basis.

Comparison. The measure is not adequate for comparing one project to another, since there are many other factors than the rate of return that should be considered, not all of which can be expressed quantitatively.

Cash flow. The measure includes all non-cash expenses, such as depreciation and amortization, and so does not reveal the return on actual cash flows experienced by a business.

Time-based risk. There is no consideration of the increased risk in the variability of forecasts that arises over a long period of time.

In short, the accounting rate of return is not by any means a perfect method for evaluating a capital project, and so should be used (if at all) only in concert with a number of other evaluation tools. In particular, you should find another tool to address the time value of money and the risk associated with a long-term investment, since this tool does not provide for it. Possible replacement measurements are net present value, the internal rate of return, and constraint analysis. This measure would be of the most use for reviewing short-term investments where the impact of the time value of money is reduced.

Similar Terms

The accounting rate of return is also known as the average rate of return or the simple rate of return.

Knowing how to calculate Accounting Rate of Return (ARR) is important in capital budgeting as it is used to determine the appropriateness of a particular investment. When the answer for ARR exceeds a specific rate, which is accepted by the company, then the project will be selected.

Formula to Calculate Accounting Rate of Return (ARR)

ARR can be calculated using the below formula:

Average Accounting profit is the mean of the accounting income that is expected to earn within the lifetime of the project. Instead of initial investment there are instances where the average investment is used.

The decision to accept or reject a project is based on the value generated in ARR. The project is accepted if the ARR value is equal to or greater than the required rate of return. In mutually exclusive projects, the project that generates the higher ARR is accepted.

Examples to calculate accounting rate of return (ARR)

Following examples illustrate the ways of calculating ARR.

E.g.1: Project A is having an initial investment of $150,000, and it is expecting to generate an annual cash inflow of $40,000 for 5 years. Depreciation is calculated based on the straight line method. The scrap value is about $20,000 at end of the 5th year.

ARR can be calculated as,

E.g.2: Compare the following mutually exclusive projects based on ARR and identify which project is financially feasible to undertake.

Project A

Since ARR of a project A is higher that of B, it is more favorable than the project B.

There are many advantages and disadvantages of ARR as indicated below:

Making Capital Investment Decisions and How to Calculate Accounting Rate of Return – Formula & Example

Before we get into How to Calculate Accounting Rate of Return let me give you a bit of introduction.

In order to make capital investment decisions businesses can use various appraisal methods such as Accounting Rate of Return (ARR), Payback Period (PP), Net Present Value (NPV) and Internal Rate of Return(IRR). Some business might use variations of all of the above models. Others, for example, small businesses might not be using any method of investment appraisal as they will rely on their manager’s experience or just a gut feeling.

Each of these appraisal methods has their own advantages and disadvantages which need to be taken into account when eventually making decisions.

Having said that, Accounting rate of return as one of the investment appraisal techniques is a percentage measuring the average annual operating profit against the average investment.

To get the required rate of return, we need to use the formula for ARR or Accounting Rate of Return below:

ARR = (Average annual operating profit)/( Average investment) x100%

In order to calculate ARR, we will use the example below.

Let’s assume that initial investment is £150.000 and estimated operating profits before depreciation are as proposed in Table 1.

To calculate accounting rate of return we first need to calculate an average annual operating profit.

If we know that: Average Annual Operating Profit = Average Annual Operating Profit Before Depreciation (over 3 years in this case) minus Depreciation Charge.

STEP 1

Before we start with calculating accounting rate of return we need to calculate an average annual operating profit before depreciation (over 3 years in this case).

Average annual operating profit before depreciation (over 3 years) = (65.000+110.000+175.000) / 3 = £116.667

STEP 2

The second step in our ARR calculation is to find the Annual depreciation charge.

Annual depreciation charge equals the initial cost of machine minus residual value divided by time period.

Annual depreciation charge = (150.000-25.000) / 3 = £41.667

STEP 3

Once we have an Average annual profit before depreciation and depreciation charge we can calculate an Average annual profit after depreciation.

An Average annual profit after depreciation equals Average annual profit before depreciation minus annual depreciation charge = 116.667 – 41.667 = £75.000

STEP 4

To get an average investment we divide the sum of initial investment and residual value with 2.

Average investment = (Initial investment + Residual value) / 2

STEP 5

Now once we have all the necessary inputs we can just plug in the numbers into our formula and we get our accounting rate of return as:

ARR= (75.000)/( 87.500) X 100 % = 85.71%

What is Accounting Rate of Return – Advantages and Disadvantages Explained

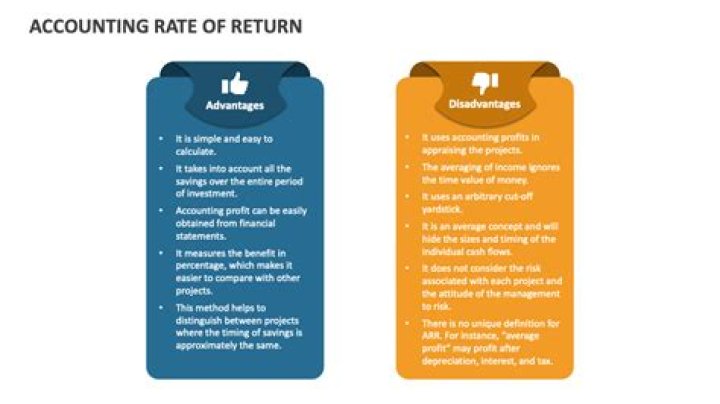

The key advantage of accounting rate of return calculation as a method of investment appraisal is that is easy to compute and understand. The results of ARR are given in percentage and that might be a preferable measure for many company managers.

The main disadvantage of Accounting Rate of Return (arr) is that it disregards the time factor in terms of time value of money or risks for long-term investments. The ARR is built on the evaluation of profits and that’s why it can be easily manipulated with changes in depreciation methods. The ARR can give completely misleading information’s when evaluating different size investments.

Watch our video explaining “How to Calculate Accounting Rate of Return [in 5 Steps]”

How to Calculate Work Days Between Two Dates

To help you manage your business investments, Microsoft Excel includes many timesaving functions, including an annual growth rate formula called internal rate of return (IRR). It automatically calculates the average annual rate of return based on a list of transaction amounts where cash flows occur regularly. A second function, XIRR, gives you annual rates of return for investments where the money is paid out at irregular intervals.

TL;DR (Too Long; Didn’t Read)

The IRR() function in Excel acts as an annual rate of return calculator for investments that pay out at regular intervals.

What is Annual Rate of Return?

The annual rate of return for an investment is the percentage change of the total dollar amount from one year to the next. If the investment made a profit, the percentage is positive. Investment losses give negative percentages.

Average Annual Rate of Return

The average annual rate of return of your investment is the percentage change over several years, averaged out per year. A bank might guarantee a fixed rate per year, but the performance of many other investments varies from year to year. It helps to average the percentage change so you have a single number against which to compare other investments.

Example Average Annual Rate of Return

As an example, a bank offers a 1.5% rate on a certificate of deposit. By comparison, a business investment may lose 2% one year but gain 6% the next. The total compounded gain for the investment is (1-.02) x (1+.06) or 3.88%. The average for 2 years is 3.88/2 or 1.94%, better than the bank rate. Note that you can’t simply average -2% and 6% together, such as (-2 + 6) / 2 or exactly 2; compounding affects the results.

Annual Rate of Return Excel IRR()

The Excel function IRR() takes a list of amounts that are usually set up in a column. For the function to work, the list must have at least one negative and one positive amount. The first negative amount represents the initial funds that went into the investment. The function assumes that cash flows occur on regular intervals, once per interval. For example, you enter the following dollar amounts into column A, starting at A1:

In A7, you enter the formula, IRR(A1:A6). These items represent an initial investment of $100,000 and payouts in the amounts that follow. Excel calculates the average annual rate of return as 9.52%. Remember that when you enter formulas in Excel, you double-click on the cell and put it in formula mode by pressing the equals key (=). When Excel is in formula mode, type in the formula.

Note that IRR() doesn’t assume that the interval is years. It could instead be months, in which case the return is 9.52% per month. The IRR() function doesn’t “know” the interval — you do.

Function for Irregular Cash Flows XIRR()

The XIRR() function works much the same as IRR(), but doesn’t assume regular cash flows. In addition to a column of amounts, you provide a second column of corresponding dates. The function calculates the average annual return based on those two sets of data. To give an example, you have these amounts and dates. The first entry represents the start of the investment:

-25,000 7/1/22

4500 11/30/22

3250 1/1/23

4500 10/31/23

5000 2/1/24

6375 7/15/24

5000 1/31/25

The amounts go into column A, starting at A1. The dates go to column B, starting with B1. Note that you can’t use dates in Excel as-is; for the math to work, you must use the date function as these examples illustrate:

In B8, the first empty cell under the dates, you enter the following equation:

Excel calculates the average annual rate of return as 0.095, or 9.5%.

An Educated Guess

Both the IRR() and XIRR() have an optional third parameter in which you can provide a “guess” value to the function. In the majority of cases, Excel can calculate the rate of return without the guess. But some sets of data present difficulties with calculations; the guess gives the software a starting point, and the function “homes in” from there. For example, if the function returns a calculation and you think the rate of return is close to 5%, use 5% for the guess, as follows:

The Advantages & Disadvantages of the Internal Rate of Return Method

Businesses can sometimes find themselves with more investment opportunities than finances. While a good problem to have, decisions have to be made as to which opportunities to pursue and which to reject. Capital budgeting deals with analyzing potential projects using tools like internal rate of return and accounting rate of return.

Internal Rate of Return

The internal rate of return (IRR) is the interest rate at which the present value of the dollars invested in a particular project would equal the present value of the cash inflows from the project. The present value means future cash discounted back to the current period. This interest rate is the break-even point. For a company to invest in the project, it would have to earn a greater return. For example, a project with a $1,100,000 investment, payments of $400,000 in Year 1 and $600,000 in Year 2 with a $250,000 salvage value would have an IRR of 8%.

Accounting Rate of Return

The accounting rate of return (ARR) is the average annual income from a project divided by the initial investment. For instance, if a project requires a $1,000,000 investment to begin, and the accounting profits are projected to be $100,000 annually, the ARR is 10%. The advantage of the ARR compared to the IRR is that it is simple to calculate.

Time Value of Money

Only the IRR takes the time value of money into account. The time value of money is the idea that money now is worth more than money in the future because it can be invested and grow. Not only does the ARR not take the time value of money into account for stable cash flows, but a project that pays out $500 in the fifth year will have the same ARR as a project that pays out $100 a year for five years (assuming the same initial investment).

Accounting Profits vs. Cash Profits

The ARR uses accounting profits while the IRR uses cash inflows. Accounting profits are subject to a number of different treatments that can affect the bottom line profits. For instance, depreciation can be calculated in different ways, such as straight-line or accelerated. It will also ignore the salvage value of the initial investment at the end of the project, such as a factory that can be sold at the end of its useful life.

What is a Rate of Return?

A Rate of Return (ROR) is the gain or loss of an investment over a certain period of time. In other words, the rate of return is the gain Capital Gains Yield Capital gains yield (CGY) is the price appreciation on an investment or a security expressed as a percentage. Because the calculation of Capital Gain Yield involves the market price of a security over time, it can be used to analyze the fluctuation in the market price of a security. See calculation and example (or loss) compared to the cost of an initial investment, typically expressed in the form of a percentage. When the ROR is positive, it is considered a gain and when the ROR is negative, it reflects a loss on the investment.

Video Explanation of Rate of Return

Watch this short video to quickly understand the main concepts covered in this guide, including the definition of rate of return, the formula for calculating ROR and annualized ROR, and example calculations.

Formula for Rate of Return

The standard formula for calculating ROR is as follows:

Keep in mind that any gains made during the holding period of the investment should be included in the formula. For example, if a share costs $10 and its current price is $15 with a dividend of $1 paid during the period, the dividend should be included in the ROR formula. It would be calculated as follows:

(($15 + $1 – $10) / $10) x 100 = 60%

Example Rate of Return Calculation

Adam is a retail investor and decides to purchase 10 shares of Company A at a per-unit price of $20. Adam holds onto shares of Company A for two years. In that time frame, Company A paid yearly dividends of $1 per share. After holding them for two years, Adam decides to sell all 10 shares of Company A at an ex-dividend price of $25. Adam would like to determine the rate of return during the two years he owned the shares.

To determine the rate of return, first, calculate the amount of dividends he received over the two-year period:

10 shares x ($1 annual dividend x 2) = $20 in dividends from 10 shares

Next, calculate how much he sold the shares for:

10 shares x $25 = $250 (Gain from selling 10 shares)

Lastly, determine how much it cost Adam to purchase 10 shares of Company A:

10 shares x $20 = $200 (Cost of purchasing 10 shares)

Plug all the numbers into the rate of return formula:

= (($250 + $20 – $200) / $200) x 100 = 35%

Therefore, Adam realized a 35% return on his shares over the two-year period.

Annualized Rate of Return

Note that the regular rate of return describes the gain or loss, expressed in a percentage, of an investment over an arbitrary time period. The annualized ROR, also known as the Compound Annual Growth Rate (CAGR) CAGR CAGR stands for the Compound Annual Growth Rate. It is a measure of an investment’s annual growth rate over time, with the effect of compounding taken into account. , is the return of an investment over each year.

Formula for Annualized ROR

The formula for annualized ROR is as follows:

Similar to the simple rate of return, any gains made during the holding period of this investment should be included in the formula.

Example of Annualized Rate of Return

Let us revisit the example above and determine the annualized ROR. Recall that Adam purchased 10 shares at a per-unit price of $20, received $1 in dividends per share each year, and sold the shares at a price of $25 after two years. The annualized ROR would be as follows:

(($250 + $20) / $200 ) 1/2 – 1 = 16.1895%

Therefore, Adam made an annualized return of 16.1895% on his investment.

Alternative Measures of Return

Return can mean different things to different people, and it’s important to know the context of the situation to understand what they mean. In addition to the above methods for measuring returns, there several other types of formulas.

Common alternative measures of returns include:

- Internal Rate of Return (IRR) Internal Rate of Return (IRR) The Internal Rate of Return (IRR) is the discount rate that makes the net present value (NPV) of a project zero. In other words, it is the expected compound annual rate of return that will be earned on a project or investment.

- Return on Equity (ROE) Return on Equity (ROE) Return on Equity (ROE) is a measure of a company’s profitability that takes a company’s annual return (net income) divided by the value of its total shareholders’ equity (i.e. 12%). ROE combines the income statement and the balance sheet as the net income or profit is compared to the shareholders’ equity.

- Return on Assets (ROA) Return on Assets & ROA Formula ROA Formula. Return on Assets (ROA) is a type of return on investment (ROI) metric that measures the profitability of a business in relation to its total assets. This ratio indicates how well a company is performing by comparing the profit (net income) it’s generating to the capital it’s invested in assets.

- Return on Investment (ROI) Return on Investment (ROI) Return on Investment (ROI) is a performance measure used to evaluate the returns of an investment or compare efficiency of different investments.

- Return on Invested Capital (ROIC) Return on Invested Capital Return on Invested Capital – ROIC – is a profitability or performance measure of the return earned by those who provide capital, namely, the firm’s bondholders and stockholders. A company’s ROIC is often compared to its WACC to determine whether the company is creating or destroying value.

More Resources

CFI is the official provider of the Financial Modeling & Valuation Analyst (FMVA) FMVA® Certification Join 350,600+ students who work for companies like Amazon, J.P. Morgan, and Ferrari certification, designed to teach valuation modeling skills to financial analysts. To continue advancing your career, these additional resources will be useful:

- Investing: A Beginner’s Guide Investing: A Beginner’s Guide CFI’s Investing for Beginners guide will teach you the basics of investing and how to get started. Learn about different strategies and techniques for trading, and about the different financial markets that you can invest in.

- Unlevered Beta (Asset Beta) Unlevered Beta / Asset Beta Unlevered Beta (Asset Beta) is the volatility of returns for a business, without considering its financial leverage. It only takes into account its assets. It compares the risk of an unlevered company to the risk of the market. It is calculated by taking equity beta and dividing it by 1 plus tax adjusted debt to equity

- Basis Points (bps) Basis Points (BPS) Basis Points (BPS) are the commonly used metric to gauge changes in interest rates. A basis point is 1 hundredth of one percent. See examples. This metric

- Technical Analysis: A Beginner’s Guide Technical Analysis – A Beginner’s Guide Technical analysis is a form of investment valuation that analyses past prices to predict future price action. Technical analysts believe that the collective actions of all the participants in the market accurately reflect all relevant information, and therefore, continually assign a fair market value to securities.

Please login to continue

Assignment detail

Reference no: EM132510866

Problem 1

The latest manufacturing equipment is purchased at a cost of $800,000. As a result, annual cash revenues are expected to increase by $345,000; annual cash expenses are expected to increase by $162,000; straight-line depreciation is used; the asset has a seven-year life; the salvage value is $100,000. Assume the company is in the new 21% corporate tax bracket.

Question 1: Determine the accounting rate of return? (round to the nearest %)

Question 2: Determine the payback period?

Question 3: Determine the NPV assuming a minimum required rate of return of 8%?

Problem 2 (Ignore taxes for this problem)

Bullock Prosthetics is planning to buy 3-D printing machinery costing $380,000. This machinery’s expected useful life is 5 years. They require a minimum rate of return of 8%, and have calculated the following data pertaining to the purchase and operation of this machinery:

Year Estimated Annual Cash Inflows Estimated Annual Cash Outflows Depreciation

1 90,000 15,000 60,000

2 150,000 45,000 60,000

3 230,000 95,000 60,000

4 270,000 110,000 60,000

5 300,000 125,000 60,000

Question 4: Determine Terra’s payback period, accounting rate of return, and NPV for this investment?

Problem 3

Z Company is planning to purchase a system capable of deploying Artificial Intelligence for monitoring the company’s transactions for accuracy and misuse. The expected cost of this system is $165,000, and it is expected to have a useful life of 6 years and an estimated salvage value of $26,500. The system is expected to produce cash savings of $57,000 per year in reduced labor costs and the cash operating costs to run this system are estimated to be $17,000 per year. Assuming Company X is in the new 21% tax bracket and has a minimum desired rate of return of 12% on this investment.

Question 5: Determine the:

(a) payback period, (b) ARR, and (c) NPV (Ignoring taxes), and(a) payback period, (b) ARR, and (c) NPV (Assuming taxes).

Related Assignments

Explain the mitigate effect of rising seas on drinking water

Reference no: EM132435005 , Length: word count :- 300 Based on what you have learned so far from this class, discuss the following: Question 1:

How coordination between preparedness programs is essential

Reference no: EM132538297 Assignment: Objectives: • Evaluate how coordination between all preparedness programs is essential, whether creating a local emergency operations plan or a family

Anyone can explain what is effective communication

Assignment Help >> Business Management Anyone can explain what is effective communication? Please list the three main types of communication skills.

Describe social bandwidth and share an experience

Reference no: EM132486599 Question: Describe social bandwidth and share an experience you’ve had with this concept within your previous interactions. Post your response to the

If you have already studied other capital budgeting methods (net present value method, internal rate of return method and payback method), you may have noticed that all these methods focus on cash flows. But accounting rate of return (ARR) method uses expected net operating income to be generated by the investment proposal rather than focusing on cash flows to evaluate an investment proposal.

Under this method, the asset’s expected accounting rate of return (ARR) is computed by dividing the expected incremental net operating income by the initial investment and then compared to the management’s desired rate of return to accept or reject a proposal. If the asset’s expected accounting rate of return is greater than or equal to the management’s desired rate of return, the proposal is accepted. Otherwise, it is rejected. The accounting rate of return is computed using the following formula:

Formula of accounting rate of return (ARR):

In the above formula, the incremental net operating income is equal to incremental revenues to be generated by the asset less incremental operating expenses. The incremental operating expenses also include depreciation of the asset.

The denominator in the formula is the amount of investment initially required to purchase the asset. If an old asset is replaced with a new one, the amount of initial investment would be reduced by any proceeds realized from the sale of old equipment.

Example 1:

The Fine Clothing Factory wants to replace an old machine with a new one. The old machine can be sold to a small factory for $10,000. The new machine would increase annual revenue by $150,000 and annual operating expenses by $60,000. The new machine would cost $360,000. The estimated useful life of the machine is 12 years with zero salvage value.

Required:

- Compute accounting rate of return (ARR) of the machine using above information.

- Should Fine Clothing Factory purchase the machine if management wants an accounting rate of return of 15% on all capital investments?

Solution:

(1): Computation of accounting rate of return:

* Incremental net operating income:

Incremental revenues – Incremental expenses including depreciation

$150,000 – ($60,000 cash operating expenses + $30,000 depreciation)

$150,000 – $90,000

$60,000

** The amount of initial investment has been reduced by net realizable value of the old machine ($360,000 – $10,000).

(2). Conclusion:

According to accounting rate of return method, the Fine Clothing Factory should purchases the machine because its estimated accounting rate of return is 17.14% which is greater than the management’s desired rate of return of 15%.

Cost reduction projects:

The accounting rate of return method is equally beneficial to evaluate cost reduction projects. The accounting rate of return of the assets that are purchased with a view to reduce business costs is computed using the following formula:

Example 2:

The P & G company is considering to purchase an equipment costing $45,000 to be used in packing department. It would reduce annual labor cost by $12,000. The useful life of the equipment would be 15 years with no salvage value. The operating expenses of the equipment other than depreciation would be $3,000 per year.

Required: Compute accounting rate of return/simple rate of return of the equipment.

Solution:

* Net cost savings:

$12,000 – ($3,000 cash operating expenses + $3,000 depreciation expenses)

$12,000 – $6,000

$6,000

Comparison of different alternatives:

If several investments are proposed and the management have to choose the best due to limited funds, the proposal with the highest accounting rate of return is preferred. Consider the following example:

Example 3:

The Good Year manufacturing company has the following different alternative investment proposals:

Required: Using accounting rate of return method, select the best investment proposal for the company.

Solution:

If only accounting rate of return is considered, the proposal B is the best proposal for Good Year manufacturing company because its expected accounting rate of return is the highest among three proposals.

Definition

Accounting Rate of Return,В shortly referred to as ARR, is the percentage ofВ average accounting profit earned from an investmentВ in comparison withВ the average accounting value of investmentВ over the period.

Accounting Rate of ReturnВ is also known as theВ Average Accounting ReturnВ (AAR)В andВ Return on InvestmentВ (ROI).

Formula

Accounting Rate of ReturnВ =В В (Average Profit / Average Book Value) %

= Total accounting profit over the investment period Г· Years of Investment

Average Book Value:

= (Initial investment + Scrap Value + Working Capital) Г· 2

OR

Average Book Value:

= (N.B.V. (year 0) + N.B.V. (year 1) + N.B.V. (year 2) + …) Г· (Years of Investment + 1)

Explanation

ARR is a measure of accounting profitability of investments.

An ARR of 10% for example means that the investment would generate an average of 10%В annual accounting profitВ over the investment period based on theВ average investment.

ARR may be compared with theВ target return on investment. Investments may be accepted if the ARR exceeds the target return. However, it is preferable to evaluate investments based on theoretically superior appraisal methods such as NPV and IRR due to theВ limitations of ARR В discussed below.

The calculation of ARR requires finding theВ average profitВ andВ average book valuesВ over the investment period. Whereas average profit is fairly simple to calculate, there are several ways to calculate the average book value of investment.

How should average book value be calculated?

One of the simplest and quickest ways of calculating the average net book value of investment assets is by finding a simple average of:

- the value of assets at the start of investment (this will be equal to the amount of the initial investment); and

- the value of those assets at the end of the investment period (this should be equal to the non-depreciated part of non-current assets (i.e. salvage value) and any current assets (i.e. working capital))

This can be summarized into the following formula:

Average Book Value:

= (Initial investment + Scrap Value + Working Capital) Г· 2

In case where subsequent investments are to be made after the initial investment, the above formula would not account for the additional investment. Instead, the average book value shall be found by adding the net book value (N.B.V.) of investment assets at the end of each year as follows:

Average Book Value:

= (N.B.V. (year 0) + N.B.V. (year 1) + N.B.V. (year 2) + …) Г· (Years of Investment + 1)

Note: Net Book Value of Year 0 will be equal to the initial investment.

You may see the example below for an illustration of how to apply the above formulas.

Example

ABC PLC is planning to invest in a 5-year project.

The initial cost of the project shall be $100 million comprising $60 million for capital expenditure and $40 million for working capital requirements.

Annual net cash flows from the project are expected to be as follows:

YearВ В В В В В В В Cash Flows $M

В В 1В В В В В В В В В В В В В В (10,000)

В В 2В В В В В В В В В В В В В В В 20,000

В В 3В В В В В В В В В В В В В В В 30,000

В В 4В В В В В В В В В В В В В В В 40,000

В В 5В В В В В В В В В В В В В В В 30,000

- Year 5 cash inflows include $10m in respect of the estimated scrap value of property, plant and equipment expected to be recovered at the end of the end of the year.

- Working capital shall be maintained at the same level throughout the investment period.

- Depreciation is to be calculated on straight-line basis.

ABC PLC’s target return on investments is 15%.

Calculate the Accounting Rate of Return for the proposed project and comment.

Solution

Accounting Rate of Return:

= (Average Profit Г· Average Book Value )%

= $12m (W1) Г· $75m (W2)

As the ARR exceeds the target return on investment, the project should be accepted.

W1: Average Profit:В

= 60 (W3) ÷ 5 =  $12m

Average Book Value:

= (100 (initial investment) + 10 (scrap value) + 40 (working capital)) Г· 2

Average Book Value:

= Sum of net book values Г· (Years of investment +1)

| Year | Cash Flows | Depreciation | Profits W3 | Net Book Value at the year end W4 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Year | Net Book Value at the year end W4 | Net Book Value at the mid-year | Working | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Year | Estimated AnnualCash Inflows | Estimated AnnualCash Outflows | Depreciation |

| 1 | $ 40,000 | $8,000 | $28,000 |

| 2 | $50,000 | $18,000 | $28,000 |

| 3 | $75,000 | $22,000 | $28,000 |

| 4 | $105,000 | $35,000 | $28,000 |

| 5 | $110,000 | $50,000 | $28,000 |

- Determine Terras payback period, accounting rate of return, and NPV for this investment?

Problem 3

Company X is planning on purchasing a 3-D printer. The expected cost of this printer is $75,000, and it is expected to have a useful life of 6 years and an estimated salvage value of $3,000. The printer is expected to produce cash savings of $23,000 per year in reduced labor costs and the cash operating costs to run this printer are estimated to be $5,000 per year. Assuming Company X is in the 34% tax bracket and has a minimum desired rate of return of 12% on this investment.

- (a) payback period, (b) ARR, and (c) NPV (Ignoring taxes), and

- (a) payback period, (b) ARR, and (c) NPV (Assuming taxes).

PLACE THIS ORDER OR A SIMILAR ORDER WITH ALL ROUND ESSAYS TODAY AND GET AN AMAZING DISCOUNT.

Finding the annual rate of return is a great way to compare different investments of different sizes and different time periods. For example, you might have held a smaller investment in a stock for six years and a larger investment in real estate for two years. To determine which investment, on average, is performing better, you need to determine the annual rate of return.

Step 1

Calculate your gain or loss by subtracting the initial value of your investment from the final value of the investment. For example, if you bought land for $200,000 and sold it for $221,000 two years later, you would subtract $200,000 from $221,000 to find you had a profit of $21,000.

Step 2

Divide the gain or loss by the original value of the investment. In this example, you would divide the $21,000 gain by the original $200,000 value to get 0.105.

Step 3

Add 1 to the step 2 result. In this example, you would calculate 1 plus 0.105 to get 1.105.

Step 4

Divide 1 by the number of years you held the investment. In this example, you would divide 1 by 2 to get 0.5 because you held the investment for two years.

Step 5

Raise the answer from step 3 to the power of the step 4 result. In this example, you would raise 1.105 to the 0.5th power to get 1.051189802.

Step 6

Subtract 1 from the step 5 result to find the annual rate of return. In this example, you would subtract 1 from 1.051189802 to get 0.051189802, or about 5.12 percent per year for the annual rate of return.

- Compute the simple rate of return for an investment project.

Definition and Explanation:

The simple rate of return method is another capital budgeting technique that does not involve discounted cash flows. The method is also known as the accounting rate of return, the unadjusted rate of return, and the financial statement method. Unlike the other capital budgeting methods that we have discussed, the simple rate of return method does not focus on cash flows. Rather, it focuses on accounting net operating income. The approach is to estimate the revenue that will be generated by a proposed investment and then to deduct from these revenues all of the projected expenses associated with the project. The net operating incomes then related to the initial investment in the project, as shown in the following formula:

Formula / Equation:

[Simple rate of return = (Incremental revenues − Incremental expenses, including depreciation

= Incremental net operating income) / Initial investment * ]

* The investment should be reduced by any salvage from the sale of old equipment.

Or, if a cost reduction project is involved, formula / Equation becomes:

[Simple rate of return = (Cost savings − Depreciation on new equipment) / Initial investment * ]

* The investment should be reduced by any salvage from the sale of old equipment.

Examples:

Example 1:

Brigham Tea, Inc., is a processor of low acid tea. The company is contemplating purchasing equipment for an additional processing line. The additional processing line would increase revenues by $9,000 per year. Incremental cash operating expense would be $40,000 per year. The equipment would cost $180,000 and have a nine year life. No salvage value is projected.

Simple rate of return = ($90,000 Incremental revenues) − ($40,000 Cash operating expenses + $20,000 Depreciation) / $180,000 Initial investment

= $30,000 / $180,000

= 16.7%

Example 2:

Midwest Farms, Inc., hires people on a part-time basis to sort eggs. The cost of this hand sorting process is $30,000 per year. The company is investigating the purchase of an egg sorting machine that would cost $90,000 and have a 15-years useful life. The machine would have negligible salvage value, and would cost $10,000 per year to operate and maintain. The egg sorting equipment currently being used could be sold now for a scrap value of $2,500.

A cost reduction project is involved in this situation. By applying the above formula, we can compute the simple rate of return as follows:

Simple rate of return = ($20,000 * Cost savings − $6,000 ** Depreciation of new equipment) / $90,000 − $2,500

* $30,000 − $10,000 = $20,000 cost savings.

** $90,000 / 15 years = $6,000 depreciation.

Criticisms/Limitations of the Simple Rate of Return:

The most damaging criticism of the simple rate of return method is that it does not consider the time value of money. The simple rate of return method considers a dollar received 10 years from now as just as valuable as a dollar received today. Thus, the simple rate of return method can be misleading if the alternatives being considered have different cash flow patterns. Additionally, many projects do not have constant incremental revenues and expenses over their useful lives. As a result the simple rate of return will fluctuate from year to year, with the possibility that a project may appear to be desirable in some years and undesirable in other years. In contrast, the net present value method provides a single number that summarized all of the cash flows over the entire useful life of the project.

I need to calculate Accounting rate of return

I know that it is Average Profit/Average investment

If project 1

Cost is 1,000,000

And cash flows are Year 0 0

Year 1 150,000

Year 2 200,000

3 300,000

4 450,000

5 500,00

Project 2

Year 0 0

Year 1 400,000

Year 2 240,000

Year 3 140,000

Year 4 40,000

Year 5 40,000

| SebastianGrey |

| View Public Profile |

| Find latest posts by SebastianGrey |

150,000 400,000

200,000 240,000

300,000 140,000

450,000 40,000

50,000 40,000

Hi,

I think that to be more specific, here is the formula:

ARR=((revenue-cost)/average capital employed)*100

In your case:

Your revenues are (Project 1: 150k+200k+300k+450k50k =1,150K – Project 2: 400k+240k+140k+40k+40k = 860k)

The average capital employed is the half of capital outlay in this case Project 1 and 2: 1,000,000/2 =500,000

Project 1 Project2

Your ARR= ((1,150,000-1,000,000)/500,000)*100= 30% —– ARR= ((860,000-1,000,000)/500000)*100 = -28%

| millionboy |

| View Public Profile |

| Find latest posts by millionboy |

Read this first: Expectations for the Homework Help board

Do not simply retype or paste a question from your book or study material

We won’t do your homework questions for you.

You were given the assignment for you to learn.

If you come up with your own answer and post it for us to critique that is within reason.

If you have some SPECIFIC questions that you couldn’t find or didn’t understand, we may help with that.

But this is your assignment, so show us you have at least attempted to complete it on your own.

| Question Tools | Search this Question | ||||||||||||||||||||||||||||||||||||||

| Hupana Running Company—Stitcher Purchase | |

|---|---|

| Annual incremental revenue | $40,000 |

| Annual incremental operating expense | $5,000 |

| Annual depreciation ($100,000/5 years) | $20,000 |

| Annual incremental expenses | $25,000 |

| Annual incremental net operating income/(loss) | $15,000 |

So the simple rate of return would be: annual incremental net operating income/ initial investment cost

$15,000/$100,000= 15% simple rate of return

So it looks like the stitcher would be a good investment! What if we change up the numbers a bit. The stitcher will still add the $40,000 to revenues, but will add $10,000 to annual operating costs and only have a useful life of three years.

| Hupana Running Company—Stitcher Purchase | |

|---|---|

| Annual incremental revenue | $40,000 |

| Annual incremental operating expense | $10,000 |

| Annual depreciation ($100,000/ years) | $33,333 |

| Annual incremental expenses | $43,333 |

| Annual incremental net operating income/(loss) | −$3,333 |

We now have a negative rate of return, so would probably pass on making this purchase. This brings home the point of how important it can be to know your numbers and do your research! Also noting, a small difference, can make a huge difference in the decision to make a capital budgeting decision, so as a manager, be clear on your information and perhaps use several of the available methods before making a final decision or before taking your analysis to your supervisor!

Share:

Business investment projects need to earn a satisfactory rate of return if they are to justify their allocation of scarce capital. The average rate of return (“ARR”) method of investment appraisal looks at the total accounting return for a project to see if it meets the target return.

An example of an ARR calculation is shown below for a project with an investment of £2 million and a total profit of £1,350,000 over the five years of the project.

The ARR for the project is 13.5% which seems a reasonable return. The project looks like it is worth pursuing, assuming that the projected revenues and costs are realistic.

A key question is – how does this return compare with the target return for investments by this business?

The main advantages and disadvantages of using ARR as a method of investment appraisal are as follows:

Advantages of ARR

ARR provides a percentage return which can be compared with a target return

ARR looks at the whole profitability of the project

Focuses on profitability – a key issue for shareholders

Disadvantages of ARR

Does not take into account cash flows – only profits (they may not be the same thing)

Takes no account of the time value of money

Treats profits arising late in the project in the same way as those which might arise early

Subscribe to email updates from tutor2u Business

Join 1000s of fellow Business teachers and students all getting the tutor2u Business team’s latest resources and support delivered fresh in their inbox every morning.

You can also follow @tutor2uBusiness on Twitter, subscribe to our YouTube channel, or join our popular Facebook Groups.

Best UK USA UAE Australia Canada China Accounting Rate of Return Problem Homework Help Service Online

Jenny Durdil Company is considering an investment of $200,000 in new equipment which will be depreciated on a straight-line basis (8-year life, no salvage value). The expected annual revenues and costs of the new product that will be produced from the equipment are

| Sales | $292,000 | |

| Less costs and expenses: | ||

| Manufacturing costs | S200,000 | |

| Equipment depreciation | 25,000 | |

| Selling and administrative | 43,900 | 268,900 |

| Income before income taxes | 23,100 | |

| Income tax expense (30%) | 6,930 | |

| Net income | $ 16,170 |

How it Works?

How it Works?

Step 1:- Want to buy solution for this. Please click on submit your assignment here and then fill all details and please mentioned product code at the end of the case. Product code is extremely important to locate your assignment. You can also mail us by keeping product code as mail subject to [email protected]

Step 2:- As soon as we received your details, we will inform you with through email about quotations of the given assignment. Requesting you to please mention your budget. Also ensure our email [email protected] should not go into your spam folder.

Step 3:- Once you agree with our price, click on pay now and pay the agreed amount and once we received the payment assignment will be delivered before agreed deadline.

Step 4:-You can also call us in our phone no. as given in the top of the home page or chat with our customer service representatives by clicking on chat now given in the bottom right corner.

Features

Our Features for Assignment Help Services

Plagiarism Free Solution

The first and foremost things that we promise to our customer is plagiarism free solution i.e. a complete and unique solution as per customer’s university requirements.

Excellent Customer Care Services

You can feel our responsiveness once you use our service. Our team of excellent and dedicated customer service representatives are always ready to provide best customer care service 24X7 . Just drop a mail to [email protected] and you can receive response in just no time.

Multiple Stage Quality Assurance

We design a unique multiple stage quality assurance team to ensure plagiarism free, original, relevant and as per customer’s requirements. We not only give importance to accurate solutions or writing but also we give equal importance to references style too.

Privacy and Confidentiality

We believe in maintaining complete privacy and confidentiality of all our clients. None of the information furnished to us is shared with anyone else.

Our Clients

We receive requests from clients all over the World. Most of our customers are from USA, UK, Australia, Canada, UAE, Muscat, Oman, Qatar, UAE, New-Zealand, France Germany etc.

Related Services

Questions

(1) Compute the annual rate of return.

(2) Compute the cash payback period.

(3) Compute the net present value assuming a 12% required rate of return.

(4) Determine the internal rate of return.

Product Code: ACC45

Looking for Accounting Rate of Return Problem Homework Help, please submit your details here with product code mentioned above.

Accounting

Question:

Exercise 24-7 Iggy Company is considering three capital expenditure projects. Relevant data for the projects are as follows. Project Investment Annual Income Life of Project 22A $240,400 $16,700 6 years 23A 273,200 20,740 9 years 24A 281,300 15,700 7 years Annual income is constant over the life of the project. Each project is expected to have zero salvage value at the end of the project. Iggy Company uses the straight-line method of depreciation. Click here to view PV table. (a) Determine the internal rate of return for each project.(Round answers 0 decimal places, e.g. 10. For calculation purposes, use 5 decimal places as displayed in the factor table provided.) Project Internal Rate of Return 22A % 23A % 24A % (b) If Iggy Company’s required rate of return is 11%, which projects are acceptable? The following project(s) are acceptable Please see if you can give me the correct answer.I have gotten the wrong answer before

————————————————

Finance

Question:

Under/Over Valued Stock A manager believes his firm will earn a 17.6 percent return next year. His firm has a beta of 1.66, the expected return on the market is 15.6 percent, and the risk-free rate is 5.6 percent. Compute the return the firm should earn given its level of risk and determine whether the manager is saying the firm is under-valued or over-valued.

————————————————

Finance

Question:

Jiminy’s Cricket Farm issued a bond with 18 years to maturity and a semiannual coupon rate of 8 percent 3 years ago. The bond currently sells for 92 percent of its face value. The company’s tax rate is 40 percent. The book value of the debt issue is $45 million. In addition, the company has a second debt issue on the market, a zero coupon bond with 12 years left to maturity; the book value of this issue is $35 million, and the bonds sell for 51 percent of par. What is the company’s total book value of debt? (Enter your answer in dollars, not millions of dollars, e.g. 1,234,567.) Total book value $ What is the company’s total market value of debt? (Enter your answer in dollars, not millions of dollars, e.g. 1,234,567.) Total market value $ What is your best estimate of the aftertax cost of debt? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) Cost of debt %

HOW OUR WEBSITE WORKS

Our website has a team of professional writers who can help you write any of your homework. They will write your papers from scratch. We also have a team of editors just to make sure all papers are of

HIGH QUALITY & PLAGIARISM FREE .

To make an Order you only need to click ORDER NOW and we will direct you to our Order Page at WriteDen. Then fill Our Order Form with all your assignment instructions. Select your deadline and pay for your paper. You will get it few hours before your set deadline.

Deadline range from 6 hours to 30 days .

Once done with writing your paper we will upload it to your account on our website and also forward a copy to your email.

Step 3

Upon receiving your paper, review it and if any changes are needed contact us immediately. We offer unlimited revisions at no extra cost .

Is it Safe to use our services?

We never resell papers on this site. Meaning after your purchase you will get an original copy of your assignment and you have all the rights to use the paper.

Discounts

Our price ranges from $8-$14 per page. If you are short of Budget, contact our Live Support for a Discount Code. All new clients are eligible for 20% off in their first Order. Our payment method is safe and secure.

Please note we do not have prewritten answers. We need some time to prepare a perfect essay for you.

Related Articles

Whether you’re doing a what-if analysis to determine how to invest your company’s money or you’re looking backwards to see how an investment performed, calculating an average annual rate of return lets you do apples-to-apples comparison against different potential investments with different lives. Because of compounding, it isn’t as simple as just taking your total return and dividing it by the number of years, though. Excel’s XIRR function not only calculates your average annual return, but also lets you do it with cash flows that come at irregular times.

Step 1

Open Excel by double-clicking its icon. Press “File,” then “New,” then “Blank workbook” to open a new spreadsheet if it doesn’t open with one by default.

Step 2

Put all of your cash flows in column A. Enter money you spend as a positive number and money that you receive as a negative number.

Step 3

Enter the date of each cash flow in the same row as the cash flow in column B using Excel’s DATE function. For instance, if your first activity was to spend $100,000 on January 1, 2012, you would put “100000” in cell A1 and “=DATE(2012,1,1)” in cell B1. If your next cash flow was the receipt of $25,000 cash flow on April 15, 2013, you would put “-25000” in cell B1 and “=DATE(2013,4,15) in cell B2.

Step 4

Below your two tables of cash flows and dates, type “=XIRR(” without the quotation marks. Use your mouse pointer to select the cash flows so that the range fills into the formula, type a comma, use your mouse pointer again to select the dates, type a close parenthesis, and press “Enter.” For example, if you had five rows of cash flows and dates, starting in cell A1, your command should say “=XIRR(A1:A5,B1:B5).” The cell shows the average annual rate of return after Excel finishes calculating it.

Step 5

Click the cell, then click the “%” button in the “Number” section of the “Home” toolbar. Excel converts the decimal return to a percentage.

some advantages and disadvantages of a questionnaire

analysis of results. It can be sobering to consider the amount of data you will generate and the time it will take to analyse. Some advantages and disadvantages of questionnaires follow. Notes on how to deal with some of the disadvantages are also provided, as are some references to more comprehensive information on questionnaires. Some disadvantages of questionnaires: Questionnaires, like many evaluation methods occur after the event, so participants may forget important issues. Questionnaires.

Free Answer , Question , Questionnaire construction 509 Words | 3 Pages

accounting

Accounting, or accountancy, is the measurement, processing and communication of financial information about economic entities. Accounting, which has been called the “language of business”, measures the results of an organization’s economic activities and conveys this information to a variety of users including investors, creditors, management, and regulators. Practitioners of accounting are known as accountants. Accounting can be divided into several fields including financial accounting, management.

Premium Big Four auditors , Enron , Financial statements 1677 Words | 6 Pages

Generally Accepted Accounting Principles

Accountants use generally accepted accounting principles (GAAP) to guide them in recording and reporting financial information. GAAP comprises a broad set of principles that have been developed by the accounting profession and the Securities and Exchange Commission (SEC). Two laws, the Securities Act of 1933 and the Securities Exchange Act of 1934, give the SEC authority to establish reporting and disclosure requirements. However, the SEC usually operates in an oversight capacity, allowing the FASB.

Premium International Financial Reporting Standards , Balance sheet , Deferral 1303 Words | 6 Pages

Accounting

“certificate of achievement for excellence in financial reporting” by the Government Finance Officers Association? What is the significance of this award? Yes, it is significant because it is the highest form of recognition in the area of governmental accounting and financial reporting, and its attainment represents a significant accomplishment by a government and its management. (Page 13) b) What are the key issues addressed in the letter of transmittal? Major initiatives in the city of Charlotte.

Premium Income statement , Annual report , Balance sheet 852 Words | 3 Pages

Accounting

to other users and doing research in various magazines. 2. User shares information risk with management. The manufacturer of a product has a responsibility to meet its warranties and to provide a reasonable product. The buyer of an automobile can return the automobile for correction of defects. In some cases, a refund may be obtained. 3. Examine the information prepared by Consumer Reports. This is similar to an audit in the sense that independent information is provided by an independent party.

Premium Firm , Opel , Certified Public Accountant 1680 Words | 6 Pages

Risk and Return

line of returns for Asset B is steeper (has greater slope) than Asset A The slopes of these lines are the betas for each asset: 2.61 for Asset B and 1.48 for Asset A. The greater beta value of Asset B signifies that it is more responsive to market factors and therefore makes it more risky than Asset A. P8-20 Interpreting Beta a. A 15% increase in market return would lead to an 18% (15% x 1.20) increase in the asset’s return. b. An 8% decrease in market return would lead.

Premium Portfolio , Financial markets , Investment 518 Words | 3 Pages

Accounting

deals’with customers – Revenue may be recognised when a number of ‘side deals’ exist that allow the customer to return the goods after the auditor leaves. (b)FR (c) – Sample all sales made during an unusually high quarter for sales – Examine a random sample of transactions during the year – Review subsequent year for abnormal amounts of returns . 3.numerous subjective accounting judgements (a)-Smootihing profits – increasing income decreasing expenses -Transfer reserves to income – Reduce.

Premium Income statement , Audit , External auditor 632 Words | 3 Pages

Accounting Ratios

Accounting ratios are relationships expressed in mathematical terms between the figures which are connected with each other in some manner. Obviously, no purpose is served by comparing two sets of figures which are not at all connected with each other. Moreover, absolute figures are also unfit for comparison. The following are the different classification of ratios: 1. Traditional classification: The traditional classification has been on the basis of the financial statement to which the determinants.

Premium Financial ratio , Financial statements , Economics 598 Words | 3 Pages

Generally Accepted Accounting Principles

set of accounting criteria used to develop medical centers financial statements are known as generally accepted accounting principles (GAAP). GAAP are a mixture of respected criteria created by Securities and Exchange Commission (SEC) and accountants. The SEC has authority granted by The Securities Act of 1933 and the Securities Exchange Act of 1934, to determine reporting and disclosure requirements. Oversight is the general functions of the SEC, granting the Governmental Accounting Standards.

Premium Generally Accepted Accounting Principles , Financial statements , Balance sheet 844 Words | 4 Pages

Accounting for Decision Making – Essay 2

Accounting for Decision Making Study Notes Introduction to Accounting (Week One) Accounting is the process of identifying, measuring and communicating economic information (transactions) of a business to a variety of users for decision making purposes. Business transactions are an external exchange of something of value between 2 or more entities. They can reliably be measured and recorded and can affect the assets, liabilities and equity of a business/ organisation. Accounting information is.

Premium Financial statements , Liability , Balance sheet 1509 Words | 7 Pages

Browse Accounting Lessons Here

Accounting Terms & Definitions

Accounting for Merchandising Activities

Debits and Credits (Double Entry Accounting)

Business Valuation Formulas

Time Value of Money & Present/Future Values

Complex Debt & Equity Instruments

Common Stock & Shareholder’s Equity

Accounting & Finance Ratios

Valuing Common Stock

Corporate Income Taxes

Lower of Cost or Market (LCM) & Inventory Valuation

Chart of Accounts & Bookkeeping

Bonds Payable & Long Term Liabilities

Capital Assets

GAAP, Accrual & Cash Accounting, Information Commodity, Internal Controls & Materiality

Explore Careers in Accounting and Finance

How to Calculate Return on Invesment (ROI)

Return on Invesment as the name suggests is a financial valuation method that determines the percent of return investors are getting from their portfolio of investments. Return on Investment is probably one of the most important ratios that companies need to keep track of in order to determine the viability & continuity of their business.Measuring profit margins of products being sold is not enough to continue doing business, companies have to ensure the amount of capital that is being put in to the business is attracting sufficient sales & providing a good return on capital invested.

As a rule of thumb, if the ROI is too low, this means the product lines are not generating enough sales worth running the business and deploying overhead costs, thus in the long term the product line is deemed to fail. The formula for Return on Investment is:

An alternative formula for ROI is:

Another formula that small investors use to calculate ROI is:

For instance, assume you are the VP of a long distance phone company that does a marketing campaign to generate new buyers of its long distance phone cards. The company sells each phone card for $5, and does an advertising campaign on the radio/television worth $500,000. This campaign helps the company sell an additional 155,500 long distance phone cards off its distribution networks. What is the ROI?

ROI = (Gain from Investment – Cost of Investment) / Cost of Investment

Gain from Investment = 155,500 cards x $5 = $777,500

Cost of Investment = $500,000

ROI = ($777,500 – $500,000) / $500,000

ROI = $277,500 / $500,000

ROI = 55.5%

That’s a pretty impressive number hey, 55.5%? Well most small business managers forget to factor in the costs they incurred to produce that extra revenue generated from the advertising campaign. For instance, say this long distance phone company incurred an extra $200,000 in costs to produce those 155,500 phone cards which includes phone network fees, vendor distribution expenses, selling & general admin expenses, etc. How will this additional information change our ROI calculation?

ROI = (Gain from Investment – Cost of Investment) / Cost of Investment

Gain from Investment = 155,500 cards x $5 = $777,500

Cost of Investment = $500,000 + $200,000

ROI = ($777,500 – $700,000) / $700,000

ROI = $77,500 / $700,000

ROI = 11.1%

Now see how drastically our ROI number changes? It drops from a whopping 55.5% to 11.1% thanks to the additional information we input. The lesson here is always be careful when calculating your Gain from Investment because most business managers forget to include the Cost incurred to obtain that gain, in our case the additional $200,000 of fixed costs incurred on top of the $500,000 we paid to radio/broadcasting networks for the advertising campaign.